What to Do With Your First $1,000

When I had my first $1,000 saved, I felt two things at once: proud…and stuck.

I knew I should do something smart with it—but I wasn’t sure what that was. Spend it? Invest it? Keep it in a savings account just in case?

Looking back, I realize how important that moment was. $1,000 might not seem like much, but it’s often your first real step toward financial independence. If you handle it right, it sets the tone for everything that follows.

Here’s exactly what I recommend doing with your first $1,000—based on what I did, what I wish I’d done, and what I’ve learned since.

Step 1: Make Sure You’re Not in Crisis Mode

Before you invest a dollar, ask yourself: Is this money truly extra?

If you’re behind on rent or don’t have groceries for the week, the answer is no. Use that $1,000 to stabilize your life first. Safety comes before strategy.

But if your basic needs are covered, here’s what comes next.

Step 2: Build a Mini Emergency Fund ($500–$1,000)

If you don’t already have an emergency fund, I suggest parking $500 to $1,000 in a high-yield savings account—not your checking account.

This isn’t forever. It’s just a cushion. A way to avoid putting a car repair or dental bill on a credit card.

If you already have a few months of expenses saved, you can skip this step.

Step 3: Pay Off Any High-Interest Debt

Credit card debt > any investment return.

If you’re paying 18–25% APR, paying that down is the best investment you can make.

Even $1,000 toward your balance will save you hundreds in future interest. This is step zero for building wealth.

Step 4: Start Investing (Even a Small Amount)

This is where it gets exciting.

Once you’re out of crisis mode and your debt is under control, even investing $100–$500 can change your life.

Here’s what I recommend for first-time investors:

- Open a Roth IRA if you’re eligible

- Buy a Total Stock Market ETF like VTI or SCHB

- Set up automatic monthly investments going forward

▶️ Not sure what an ETF is? Here’s a quick explanation.

▶️ Ready to invest $100? Start here.

Step 5: Start Thinking Long-Term

Once your first $1,000 is working for you, the real game begins.

You’ve proven you can save. Now focus on consistency.

- Can you invest $100/month?

- Can you boost your income with a side hustle?

- Can you avoid lifestyle creep as you earn more?

These are the things that build real wealth.

My Story

When I had my first $1,000 saved, I didn’t invest it. I sat on it. For months.

I was afraid of doing the wrong thing, so I did nothing. And it cost me time—arguably the most valuable part of investing.

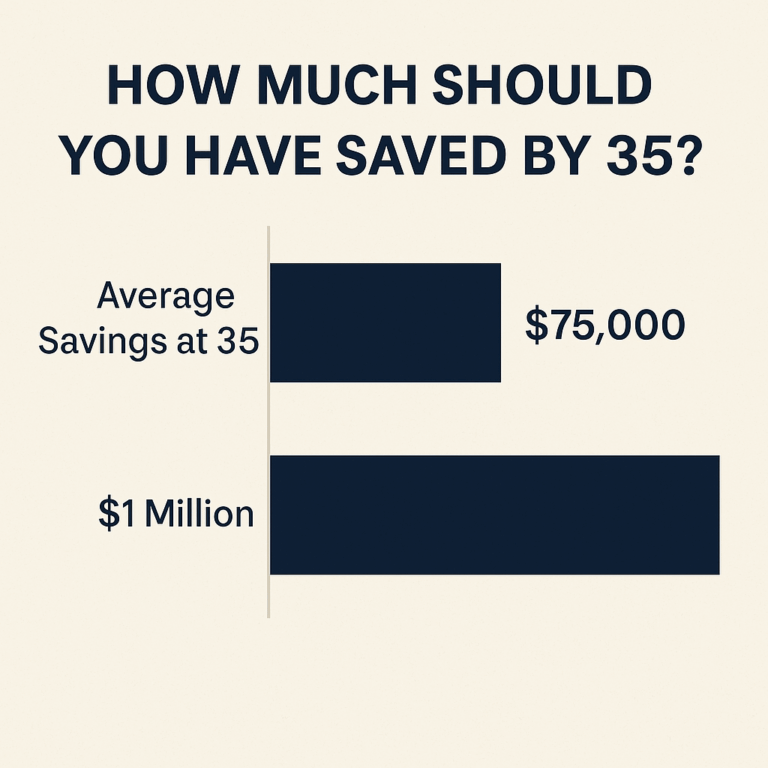

Eventually, I started investing small amounts into index funds. It wasn’t flashy. But that slow, steady approach helped me reach $1 million net worth by age 35.

That first $1,000? It mattered. It always does.

Bottom Line: What Should You Do?

Here’s the quick version:

| Situation | What to Do |

|---|---|

| Behind on bills | Use the money to catch up |

| No emergency fund | Set aside $500–$1,000 in savings |

| Carrying credit card debt | Pay it down aggressively |

| Ready to invest | Open a Roth IRA and buy a broad-market ETF |

| Want to grow long-term | Set up monthly contributions and stick with it |

Ready to Start Investing?

The most important move is your next one.

👉 Read this next: If You Only Do One Thing — Invest in a Total Stock Market ETF

👉 Or check out 10 Easy Things You Can Do Right Now to Start Investing

How I Invest My $200,000 Salary (Step-by-Step Breakdown)

I Make $200,000 a Year — Here’s How I Invest It I wasn’t always a high earner. My first job…

Weekly vs Monthly Investing: Which Is Better for Beginners?

If you’re wondering whether to invest weekly or monthly, you’re not alone.One of the most common beginner questions I get…

Saving vs Investing: What Should You Do First?

If you’re just getting started with money, you’ve probably asked this question: Should I save first, or start investing right…

What Is Dollar-Cost Averaging? (And Why It Works So Well for Beginners)

We started investing in 2013, right after I landed my first “real” job — $15 an hour, entry-level. My wife…

How to Get Rich From Nothing (Even If You’re Broke Right Now)

I started with nothing. No inheritance. No stock tips. No trust fund. My parents didn’t leave me a dime, and…

The Best First Investments for Kids (And How I’m Building Generational Wealth for My Daughter)

When I was growing up, no one handed me a roadmap to building wealth. My parents weren’t investors. They didn’t…

How Much Should You Save at 35? (Here’s What I Did)

The Short Answer: It Depends. But Let Me Tell You What Worked for Me. When I turned 35, I had…

From $0 to $1 Million by 35: A Simple Wealth-Building Strategy

TL/DR: I worked hard to steadily increase my income over time until I could save half of it every month…

If You Only Do One Thing — Invest $100 In a Total Stock Market ETF

If you’re feeling overwhelmed about investing and don’t know where to start, let me make it dead simple: Open a…